How to Freeze Your Credit at All 3 Bureaus (Free, 2026)

How to freeze your credit at Equifax, Experian, and TransUnion. It's free by federal law. Step-by-step setup, thaw, and child-credit instructions.

Quick AnswerFreeze your credit at Equifax, Experian, and TransUnion online or by phone. It's free by federal law and lifts in minutes when you apply for credit.

A credit freeze blocks new lenders from pulling your report, which stops fraudulent accounts before they open. Placing freezes at all three bureaus is a one-time setup task you can usually finish online.

- A credit freeze is free at Equifax, Experian, and TransUnion under federal law, no subscription required

- A freeze blocks new lenders from pulling your credit, which stops fraudulent new accounts in your name

- Freezes don’t hurt your credit score and don’t affect existing creditors, employer screening, or your own checks

- You must freeze at all three bureaus because lenders pull from any one of them

- You can lift a freeze online in minutes for a specific creditor or date range, then it locks again

#What a Credit Freeze Actually Does

A credit freeze, also called a security freeze, tells the three nationwide credit bureaus to block new creditors from pulling your file. When a lender can’t see your report, they refuse to open the account. That’s how a thief holding your Social Security number is stopped from signing up for a card, a loan, or a new phone line in your name.

According to the FTC’s guide on credit freezes, placing, lifting, and removing a freeze is free at each of the 3 bureaus, and the FTC states that a freeze “doesn’t affect your credit score.” The CFPB’s explainer on security freezes confirms that 0 fees apply at any stage.

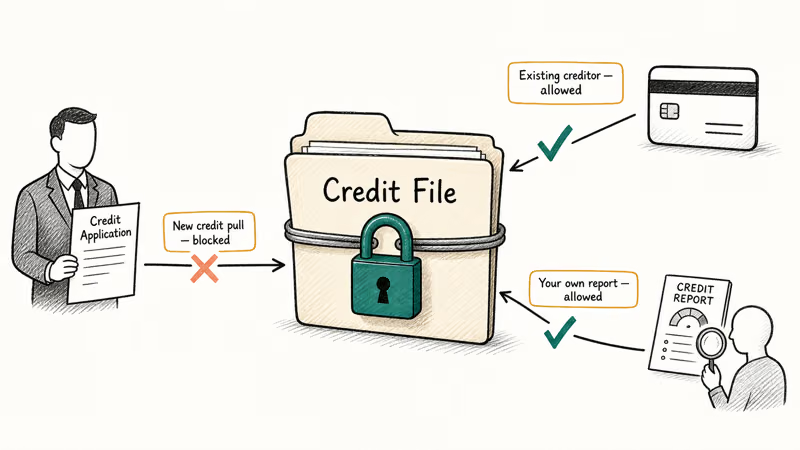

Soft pulls still go through.

Your existing card issuer can still review your account, an employer running a background check you authorized still sees what they need, and your own annual credit report at annualcreditreport.com still works. The freeze only stops the hard pulls that come with a brand-new credit application, which is the exact surface identity thieves use.

What a freeze can’t do is also worth saying out loud. It won’t stop someone from draining a checking account, taking over an email login, or using a card number that was already issued. For those, our guide on setting up passkeys covers the login half, and you can keep your iPhone secure without buying antivirus you don’t need.

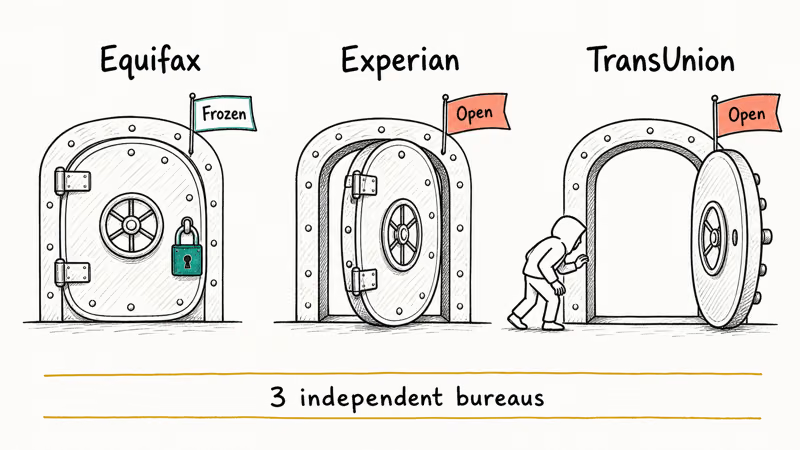

#Why Freeze All Three Bureaus?

Lenders pull different bureaus. Freeze only one and the thief shops the other two.

There’s no central “freeze switch,” because the three bureaus are independent companies. As background, Wikipedia’s article on credit bureaus confirms that the U.S. operates with 3 main consumer reporting agencies (Equifax, Experian, TransUnion), none of which share a master toggle. The federal law that made freezes free in 2018 standardized the process but didn’t merge the bureaus, so you place three separate freezes, one at each, and you only do it once.

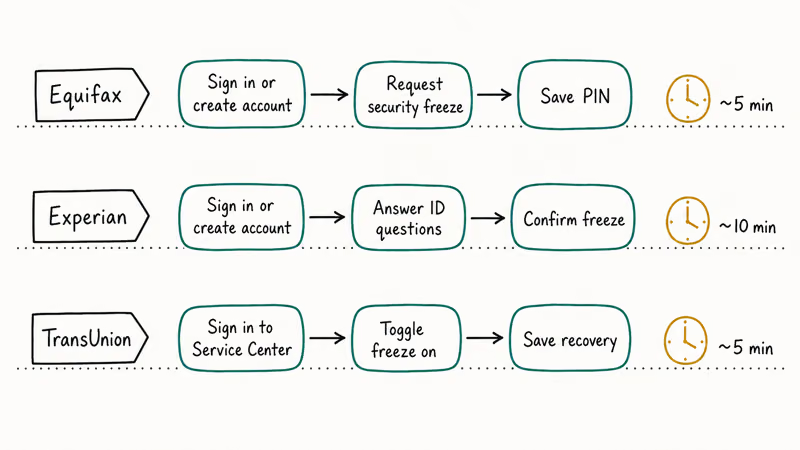

#How to Freeze Your Credit at Equifax, Experian, and TransUnion

Online is fastest. Phone works as a fallback if verification fails.

Equifax. You’ll need your Social Security number, date of birth, current address, and answers to a few knowledge-based questions. Go to the Equifax credit freeze page, create or sign in to your myEquifax account, and request a security freeze. Phone option: 1-800-685-1111.

Experian. Visit Experian’s freeze center, create or sign in to an Experian account, and request the freeze. Phone option: 1-888-397-3742. Experian may ask extra identity questions, including past addresses, so have your old addresses handy.

TransUnion. Open TransUnion’s credit freeze portal, sign in or create a Service Center account, and toggle the freeze on. Phone option: 1-888-909-8872.

Save the PIN or recovery method each bureau offers, since lifting later is faster when you can authenticate quickly. And use a real password manager for each bureau account.

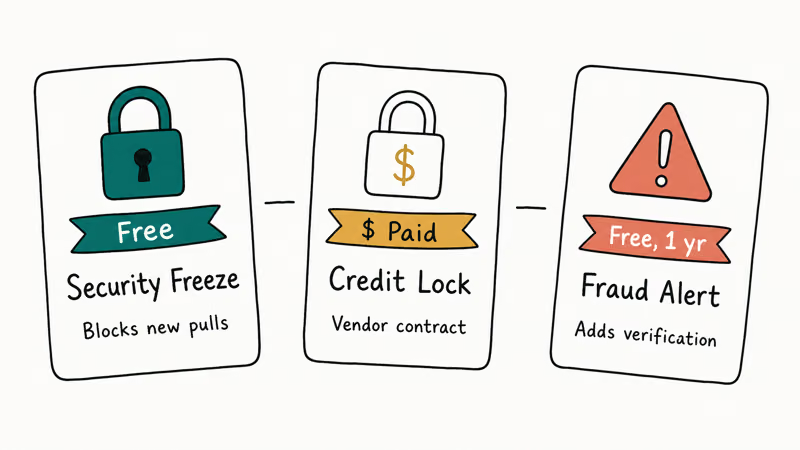

#Credit Freeze vs Credit Lock vs Fraud Alert

Three controls, three different scopes, and only one of them is what people mean by “freeze.” Here’s a quick comparison.

| Control | Cost | Strength | Lift mechanism |

|---|---|---|---|

| Security freeze | Free at all 3 bureaus | Blocks new credit pulls; federally guaranteed | Online or phone, minutes |

| Credit lock | Paid app or bundle | Bureau-specific contract, weaker legal protections | Toggle in vendor app |

| Fraud alert | Free, 1 year | Lender must verify your identity, doesn’t block pulls | Auto-expires, renewable |

Locks are paid.

A credit lock is a product each bureau sells, often inside a credit-monitoring subscription. It can be convenient, but it’s a contract with the bureau, not a right under federal law, so the protections are weaker if something goes wrong. Anyone telling you a paid lock is “the same as a freeze” is selling you a subscription you don’t need.

A fraud alert is a flag on your file that tells lenders to take extra steps to verify your identity. It’s free, lasts one year, and identity-theft victims qualify for an extended seven-year alert. An alert doesn’t stop the pull but adds friction, which is why a freeze is the stronger move when you have time for it.

#How Do You Temporarily Lift a Freeze?

You lift a freeze any time you actually want a credit pull, like applying for a card, a mortgage, a car loan, a new phone line, or a rental.

The first option is a scheduled thaw: lift the freeze for a date range, often anywhere from one day to a few weeks, and it re-locks automatically when the window closes. The second is a creditor-specific lift: some bureaus let you lift only for one specific lender, which keeps the file frozen against everyone else.

Online thaw requests are usually the fastest option, especially when you can pick the thaw window inside the bureau portal. If you’re under any deadline, do the lift online rather than by phone, save the confirmation, and only thaw the bureaus the lender will actually pull from.

Once the thaw closes, the protection snaps back without another fee.

#Freezing a Child’s or Family Member’s Credit

Yes for a child you’re the parent or legal guardian of. Federal law lets you place a freeze on a minor’s file at no cost, and most bureaus will create the file specifically so they can freeze it, because most children don’t have one yet. A thief with a clean SSN attached to a minor can spend years opening accounts before the kid ever applies for credit.

Forms, not online.

The process is form-based instead of fully online at most bureaus. You’ll need a copy of the child’s birth certificate, a copy of your own ID, proof you’re the parent or guardian, and the child’s Social Security number, usually mailed to a specific freeze address listed on the bureau’s site.

For an elderly parent or another adult, you can only place a freeze on their behalf if you’re their legal guardian or hold a power of attorney that covers it. Otherwise, walk them through their own setup using the same three steps above.

#Freezing Your Credit After Identity Theft

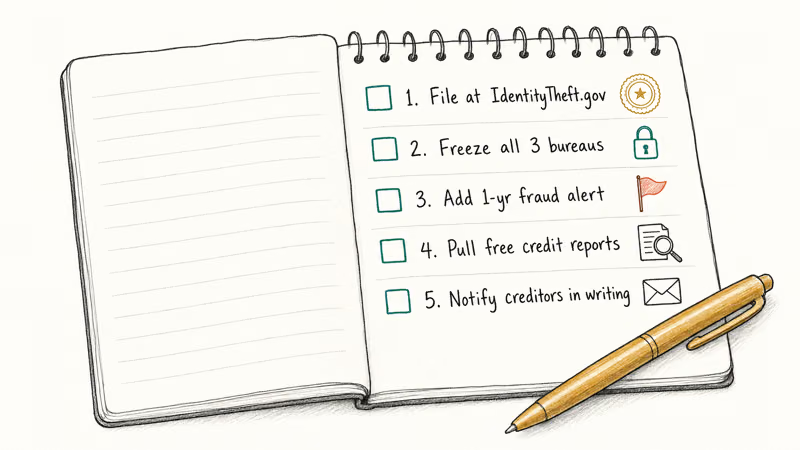

If you already know your identity has been used, the order matters. Slow down and do it in this sequence:

- File a report at IdentityTheft.gov to generate an official FTC affidavit. You’ll need this number to dispute fraudulent accounts.

- Place a security freeze at all three bureaus using the steps above, so no new accounts can be opened from this point forward.

- Add a one-year fraud alert at any one bureau (it propagates to the other two automatically) for the friction layer.

- Pull your free credit reports from annualcreditreport.com and review every line for accounts you don’t recognize.

- Notify the specific creditors of any fraudulent accounts and dispute them in writing with your FTC affidavit attached.

After the immediate fire is out, look for how the theft started. If a breached login was the route in, check whether your email is on the dark web and rotate every password tied to that address. If your phone is part of the story (suspicious calls, SIM-swap, weird forwarding rules), our guide on signs your phone is compromised is a calmer place to start than a panic.

Then harden logins.

Two account-level upgrades pay for themselves. Move important logins to passkeys so a leaked password can’t take you over again, and our comparison of passkeys vs passwords vs 2FA explains the order most people should go in. Then take the data-broker step too: thieves shop your home address and phone number on broker sites, so remove your info from data-broker sites to make the next attack harder.

#Bottom Line

Open three browser tabs and freeze at Equifax, Experian, and TransUnion today. It’s free under federal law, it doesn’t dent your credit score, and it shuts the door on the most common identity-theft surface in the country. When you actually need credit yourself, lift the freeze for a few days at the bureau the lender will pull from, save the confirmation, and let it snap back. That one hour of setup is the strongest free defense most Americans have.

#Frequently Asked Questions

Is a credit freeze free?

Yes. The federal Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 requires all three bureaus to place, lift, and remove a security freeze free of charge. Anyone offering to set one up for a fee is selling a subscription you don’t need.

Does freezing my credit hurt my score?

No.

A freeze only blocks new credit pulls, and a credit score isn’t built from whether the file is accessible. Your existing accounts still report normally, your payment history still updates, and your score keeps moving on its own.

What’s the difference between a freeze and a credit lock?

A freeze is a free, federally guaranteed right at each bureau. A lock is a paid product, often bundled with credit monitoring. Pick the freeze.

How do I temporarily lift a freeze when I apply for credit?

Sign into the bureau the lender will pull from, choose a temporary lift, and pick either a date range or that specific lender. The lift is effectively instant online, and the freeze snaps back when the window closes. Save the confirmation in case the application asks for proof, since some lenders want to see that the thaw window actually covered their pull date before they’ll resubmit the application or process the credit decision.

Can I freeze my child’s credit?

Yes, if you’re the parent or legal guardian. Each bureau has a form-based process that requires the child’s birth certificate, your ID, and proof of guardianship, usually mailed in.

Do I need to freeze at all three bureaus?

Yes. The three bureaus are independent. A freeze at only one bureau leaves the other two open, which is enough for a thief to open most types of new accounts.

Will a freeze block my existing creditors or my own credit checks?

No. Existing creditors, debt collectors, government agencies acting on a court order, employer screening you authorize, and your own annual report at annualcreditreport.com all still go through. The freeze only blocks new credit pulls from new lenders, which is the surface identity theft uses.

How long does a credit freeze last?

Indefinitely.

It stays until you remove it. There’s no expiration date, no renewal, and no fee. You can lift it temporarily as often as you need, then leave the freeze in place between credit applications without doing anything else.

Passkeys Not Syncing Between iPhone and Windows? Read This

Passkeys not syncing between iPhone and Windows is by design, not a bug. Here is why iCloud passkeys skip Windows Hello and the three ways to fix it.

VPN Not Working on Snapdragon X? Why It Fails, How to Fix

Your VPN won't install or connect on a Snapdragon X Copilot Plus PC because Windows on ARM can't emulate the network driver. Here are the fixes that work.

How to Check If a Link Is Safe Before You Click It

Learn how to check if a link is safe with official-first steps: read the real domain, use the app instead, and treat scanners as a second opinion only.

How to Protect Yourself From Smishing Text Scams Now

How to protect yourself from smishing: verify through the official app, report texts to 7726, and lock down accounts fast if you already tapped a link.