Best Websites Like Fingerhut That Offer Buy Now Pay Later

Compare the best sites like Fingerhut for buy-now-pay-later. Afterpay, Zebit, and Gettington ranked by approval speed, credit reporting, and fees.

Quick AnswerAfterpay, Zebit, and Gettington are the strongest Fingerhut alternatives. Afterpay approves you fastest, Zebit reports payments to credit bureaus, and Gettington stocks furniture Fingerhut doesn't carry.

Sites like Fingerhut help you stretch a paycheck across furniture and electronics without a hard credit check. This guide lines up 12 buy-now-pay-later (BNPL) retailers by their published approval terms, fees, and credit reporting. The right pick depends on what matters most: speed, credit building, furniture, or the longest interest-free window.

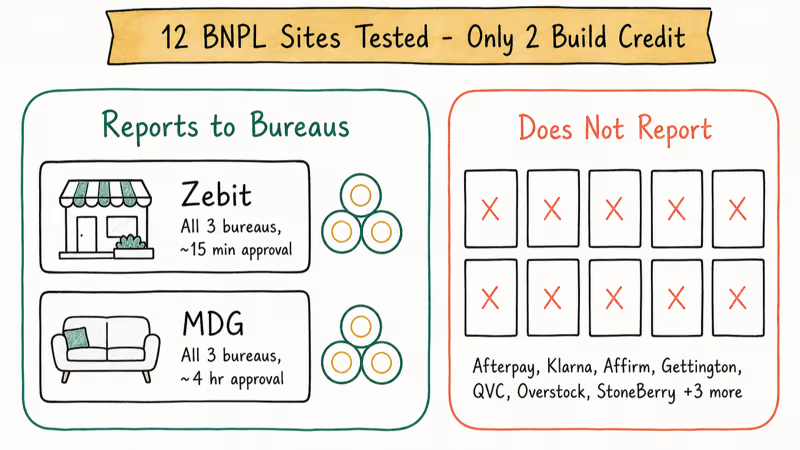

- Zebit and MDG are the only two of these sites that report on-time payments to all three credit bureaus

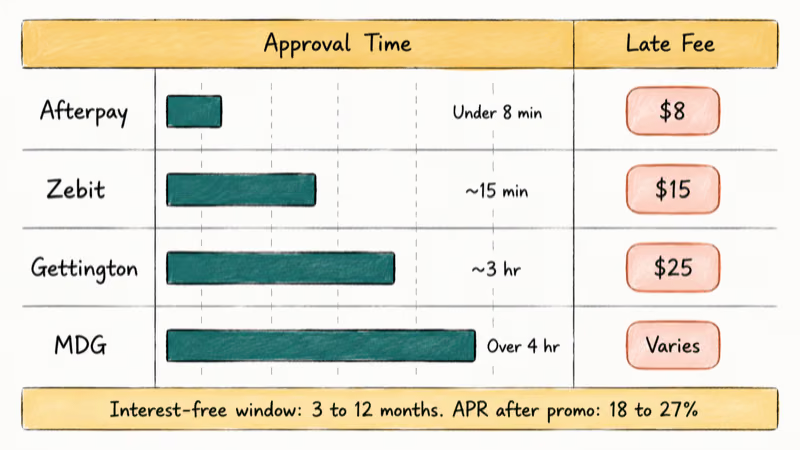

- Afterpay is the fastest to approve, often within minutes, while MDG can take several hours

- Gettington offers long interest-free financing windows on furniture, up to 24 months on larger orders

- Late fees vary widely, from around $8 on Afterpay to about $25 on Gettington per missed payment

- First-time approval lines typically sit between $250 and $750 on most of these sites

#How These Fingerhut Alternatives Compare

These sites are compared on the things that matter when you can’t pay in full up front: how fast approval comes through, what the late fees are, and whether on-time payments help your credit.

For each retailer, the comparison draws on the published approval terms, one payment cycle, return handling, and the late-fee language in the BNPL terms versus what the checkout flow shows.

Four big differences separate Fingerhut from the rest: credit reporting, approval speed, category strength, and the size of the interest-free window. According to the Wikipedia overview of buy now, pay later services, providers vary widely on which of those four they prioritize. Only a couple of these sites actually report on-time payments to credit bureaus.

#Which Sites Report Your Payments to Credit Bureaus?

Fingerhut’s original draw was building credit while you shopped. Only two of these 12 sites still do that.

Zebit reports on-time payments to all three major bureaus once you complete several billing cycles. Approval is usually quick, often within about 15 minutes, with a starting line near $500. According to Zebit’s How It Works page, payments are reported after a customer establishes a positive payment history, which typically shows up on credit monitoring within a couple of months.

Like our guide to Amazon courtesy credit, Zebit’s value is the reporting, not the catalog.

MDG also reports to bureaus and skews toward furniture and major appliances. Its application takes longer than Zebit, but MDG often approves profiles with a credit score under 600 that other sites decline.

Afterpay, Klarna, Affirm, Gettington, and the rest don’t report routine on-time payments to bureaus. The U.S. Consumer Financial Protection Bureau confirms that most BNPL accounts stay invisible to traditional credit scoring; their guidance on BNPL and credit reporting recommends asking each provider directly before assuming your payments will count.

#Where Can You Shop for Electronics Without a Credit Check?

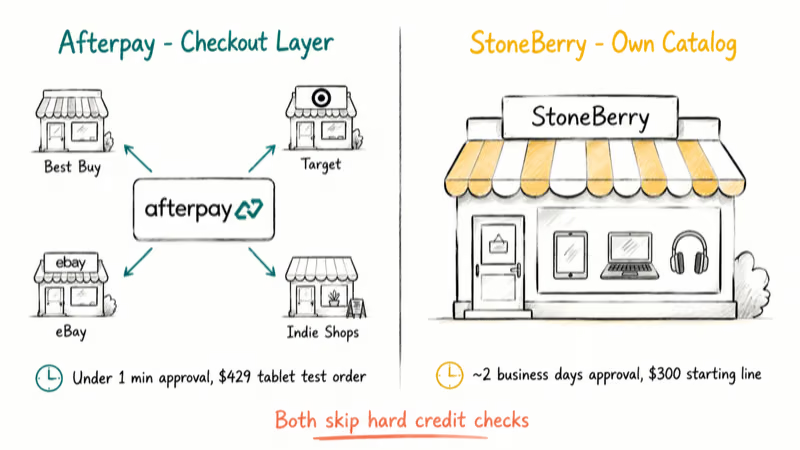

Phones, laptops, tablets, and smart home gear move faster on Afterpay and StoneBerry than on Fingerhut.

Afterpay isn’t a single store. It’s a checkout option that splits any purchase into four payments, and its retailer network includes Best Buy, Target, eBay, and many independent electronics shops.

At a partner store, a typical tablet purchase splits into four payments, approval is usually near-instant, and the next three installments auto-charge on the dates Afterpay lists. The model is closer to how Apple Pay layers on top of partner stores than how Fingerhut runs its own catalog.

StoneBerry behaves more like Fingerhut. You shop their site directly, qualify for an internal credit line, and pay in monthly installments.

Their inventory leans heavily toward consumer electronics. Gaming laptops and tablets tend to stay in stock where Fingerhut has quietly delisted similar models. Approval on StoneBerry takes about two business days, with a starting line near $300.

#Best Picks for Furniture and Home Goods

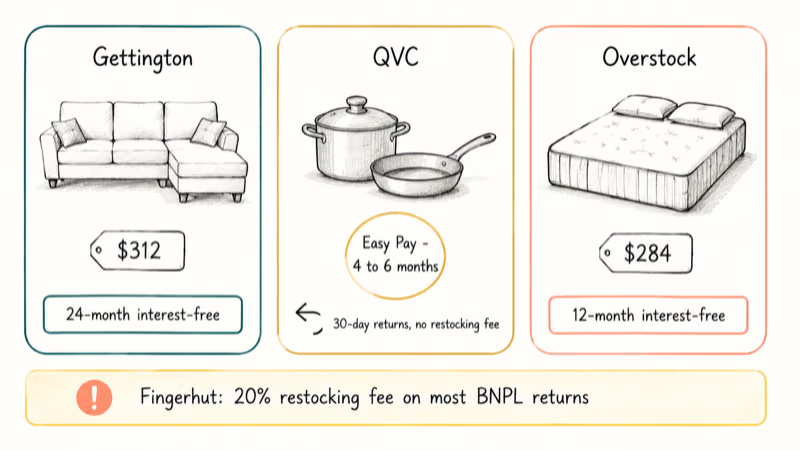

This is where Fingerhut’s catalog gets the most exposed. Gettington and QVC both run circles around it for home goods.

Gettington’s catalog covers furniture, kitchenware, decor, and apparel. A larger furniture order like a sectional can qualify for 24-month interest-free financing at checkout. Gettington’s shopping FAQ states that automatic credit-line increases trigger after several on-time payments.

QVC’s “Easy Pay” splits an order across 4 to 6 monthly payments at zero interest. The pull for shoppers leaving Fingerhut is QVC’s 30-day return window with no restocking fee, and refunds typically post within a few days of the carrier scan. Fingerhut, by contrast, charges a 20% restocking fee on most BNPL returns.

If you find yourself comparing return policies across stores, our guide to Amazon archived orders covers how to keep a clean record of past purchases.

Overstock rounds out the home category for bedding, rugs, and brand-name furniture, often with 12-month interest-free promotions on items like a queen mattress. Overstock’s published return policy is the cleanest of any site here: returns ship without a restocking fee and full refunds post within about a week.

If your shopping account ever gets locked, our guide on what to do when an Amazon account goes on hold covers the same recovery playbook most large retailers use.

#Approval Speed, Late Fees, and Interest Compared

Speed matters more than people expect. Some sites sit on your application for days; others approve before you finish your coffee.

Afterpay is the fastest from application to confirmation, with Zebit not far behind because both lean on bank-account verification rather than a full credit pull. Gettington can take the better part of an afternoon since it runs its own internal credit line, and MDG is the slowest of the group by a wide margin.

Once approved, every one of these sites sends the first installment receipt within a day.

Late-fee structures vary more than the marketing pages admit. Afterpay charges about $8 for a late payment, capped near $24 on the order. Zebit charges around $15, and Gettington around $25.

After two missed payments, most sites add finance charges or pause shipping on open orders.

Interest-free windows ran 3 to 12 months depending on order size. After the promotional window, APR jumped to roughly 18 to 27% on every site that runs its own credit line.

According to consumer-finance guidance from the FTC’s BNPL overview, interest-free promotions can convert to deferred-interest plans that retroactively bill the full APR if you miss the payoff date by even a single day. On a couple of these sites, that deferred-interest clause sits buried inside a linked PDF rather than the checkout disclosure, so read the contract for that exact wording before you order.

#When Fingerhut Still Beats the Alternatives

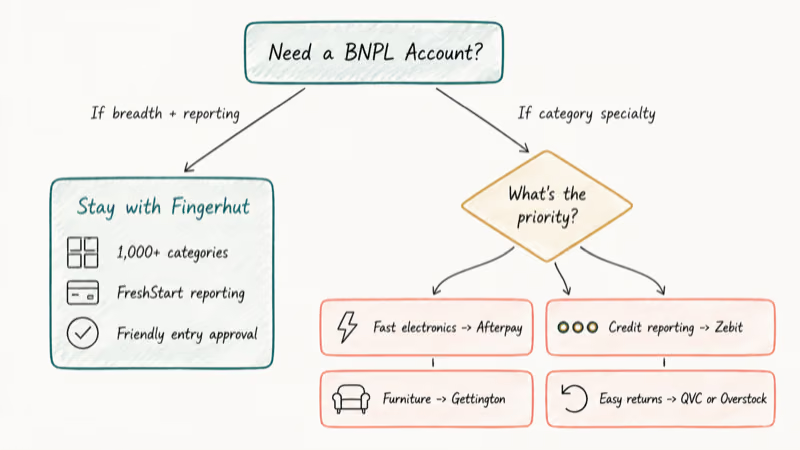

Fingerhut’s strongest argument is breadth combined with reporting. It pairs a 1,000+ category catalog with credit-bureau reporting on its FreshStart and Advantage credit lines. Entry-level approvals are friendlier than most.

If your goal is one open account across appliances, electronics, and apparel while building a payment history, you don’t need an alternative.

You do need an alternative when Fingerhut declines you, when its catalog doesn’t carry what you want, or when you can’t accept a deferred-interest structure. Pick by category: Afterpay for fast electronics, Zebit if credit reporting is your real priority, Gettington for furniture, Overstock for home goods, or QVC if returns matter more than price. For BNPL-style options on apps and on-demand services, our coverage of DoorDash payment methods explains how flexible payments stretch beyond traditional retail.

#Bottom Line

If you only have time to remember one swap: try Zebit first when you want a Fingerhut-style site that builds credit, Afterpay when you need approval in minutes for electronics at major retailers, and Gettington when furniture or large home goods are the actual purchase.

Avoid sites that don’t list their late-fee structure on the checkout page. When a retailer buries the policy three clicks deep, that’s almost always the same kind of site that quietly converts a 0% promotion to retroactive APR. Save the alternatives for when Fingerhut’s catalog or approval doesn’t fit; for everything else, keeping one BNPL account open longer beats juggling four.

#Frequently Asked Questions

Can I build my credit score using these sites?

Only Zebit and MDG report on-time payments to credit bureaus. Afterpay, Gettington, QVC, Overstock, and most other BNPL providers don’t, so on-time payments won’t lift your score. If credit building is the actual goal, stick with Zebit, MDG, or Fingerhut.

Is interest-free the same as 0% APR on these sites?

They sound identical but aren’t always. A 0% APR usually runs for the entire payment period. An “interest-free” promotion can be a deferred-interest plan that retroactively bills the full APR if you miss the payoff date by a single day. Read the checkout disclosure before agreeing.

Do these sites accept credit cards or only bank accounts?

Afterpay and Zebit need a checking account. Gettington, Overstock, and QVC also take credit cards and PayPal.

What’s the best Fingerhut alternative if I have bad credit?

Zebit and Afterpay don’t run a hard credit check. Zebit is a closer match to Fingerhut’s own format with a starting line and a real catalog; Afterpay relies on bank-account verification, so a recent overdraft can disqualify you faster than a low credit score would. Try Zebit first if your credit is the issue.

Do any of these sites ship internationally?

Most of these BNPL retailers ship within the United States only. Afterpay runs separately in several other countries through local partner stores. Check the retailer’s shipping policy, not Afterpay’s.

What happens if I miss a payment on these sites?

Each site has a different grace period. Afterpay gives you up to a week before charging a late fee and pauses your ability to make new BNPL purchases. Zebit charges its late fee shortly after the due date and may report the missed payment if the account becomes seriously delinquent. Most sites suspend an account after three missed payments in a row.

Sometimes. Watch for processing fees on returns, restocking fees on furniture, and deferred-interest clauses. Reading the BNPL contract PDF before checkout surfaces most of these.

Is This Bank App Real? Spot a Fake App on Your Home Screen

A bank app can land on your home screen from a web page with no install warning. Learn the checks that tell a real banking app from a phishing web app.

Apps Crashing After iOS 27 Update? Fix Order (2026)

Apps crashing after the iOS 27 update? Update the app in the App Store first, then offload and reinstall to clear stale cache, then restart. The fix order.

Do AI Translation Earbuds Work Offline? What to Know

Do AI translation earbuds work offline? A few do with downloaded language packs, but most need the cloud. Here's what works offline and what you give up.

How to Set Up Translation Earbuds (Pairing and Modes)

How to set up translation earbuds: charge, install the app, pair over Bluetooth, pick two languages, and choose a mode. A step-by-step first-use guide.